Collars And Price Floors Caps

Calpine Energy Solutions Products Price Collars

Http Janroman Dhis Org Stud Ii2008 Caps And Floors Pdf

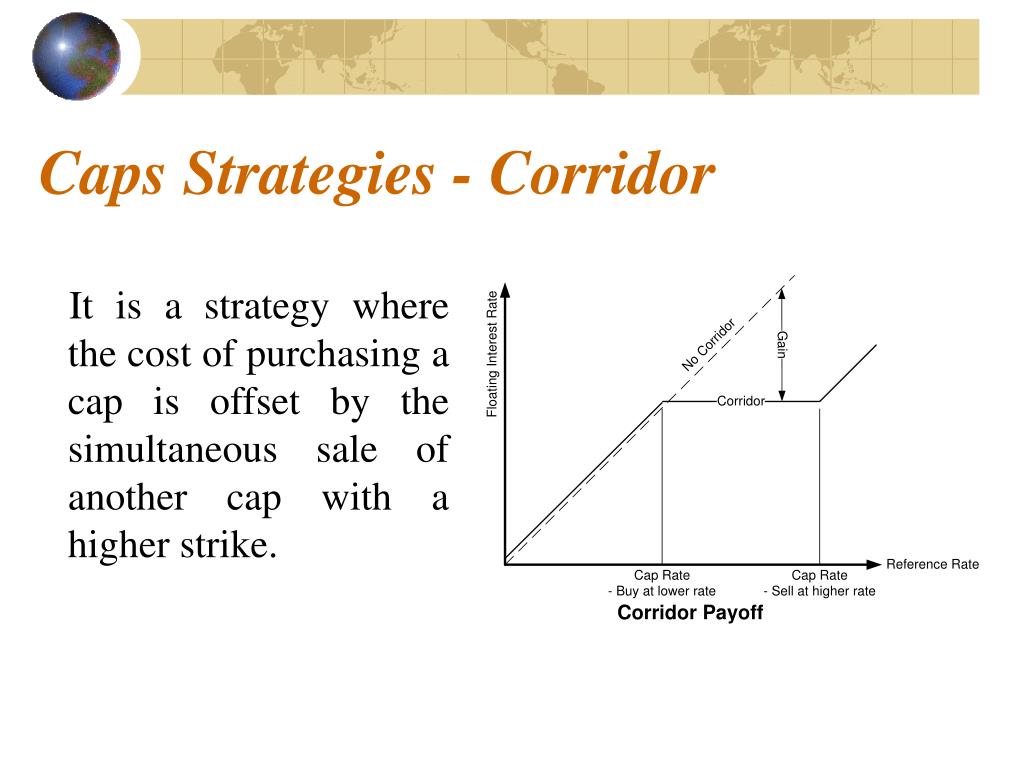

Ppt Caps Floors And Collars Powerpoint Presentation Free Download Id 6803699

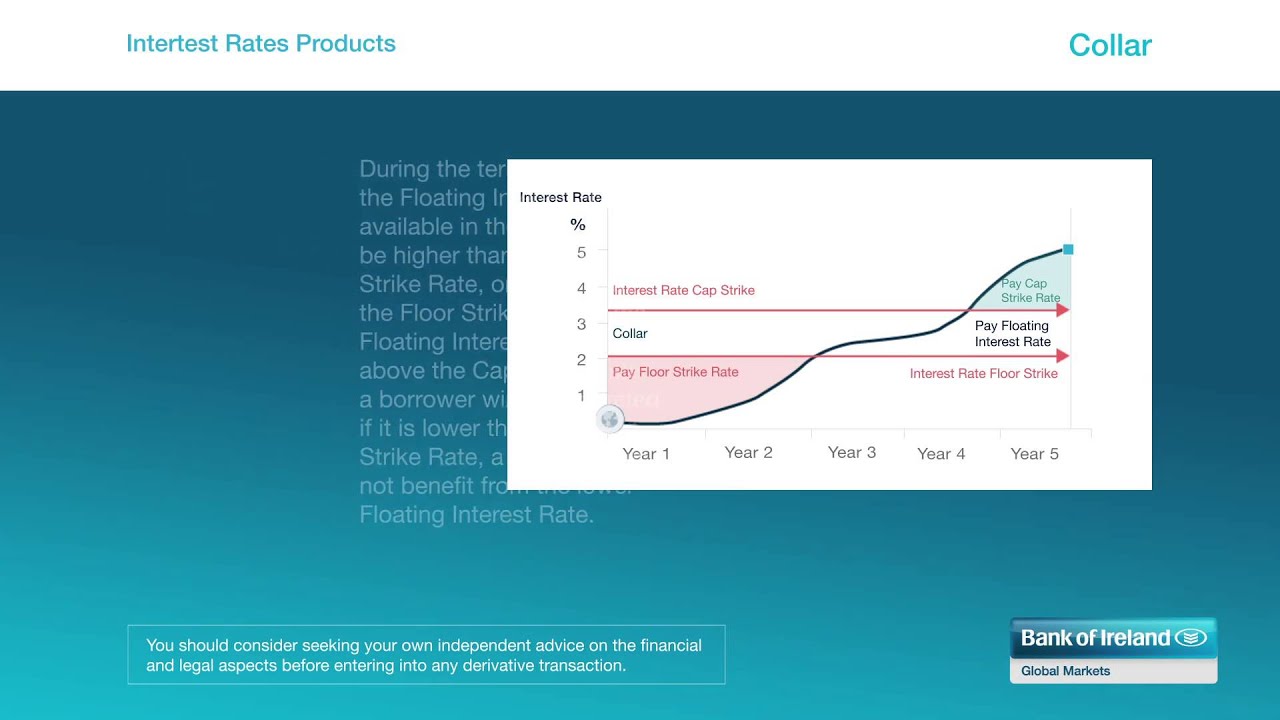

Interest Rate Products Caps Collars Youtube

:max_bytes(150000):strip_icc()/strategy-4086857_19201-23485cf7c4bf4dbbb95c93f267285f16.jpg)

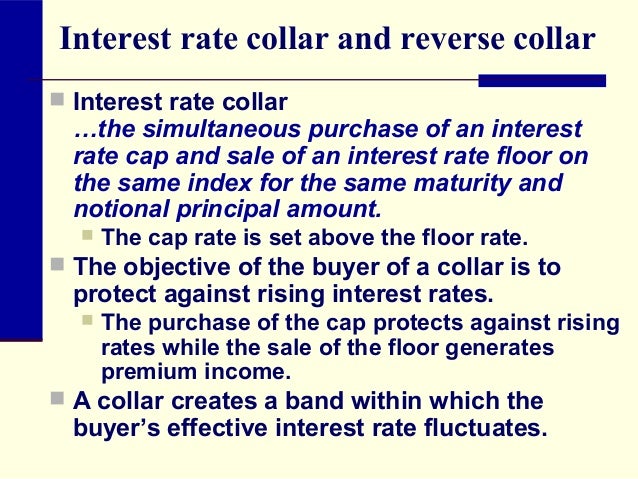

Interest Rate Collar Definition

Multi Period Options Interest Rate Caps Interest Rate Floors Ppt Video Online Download

Underlying risk reversal collar.

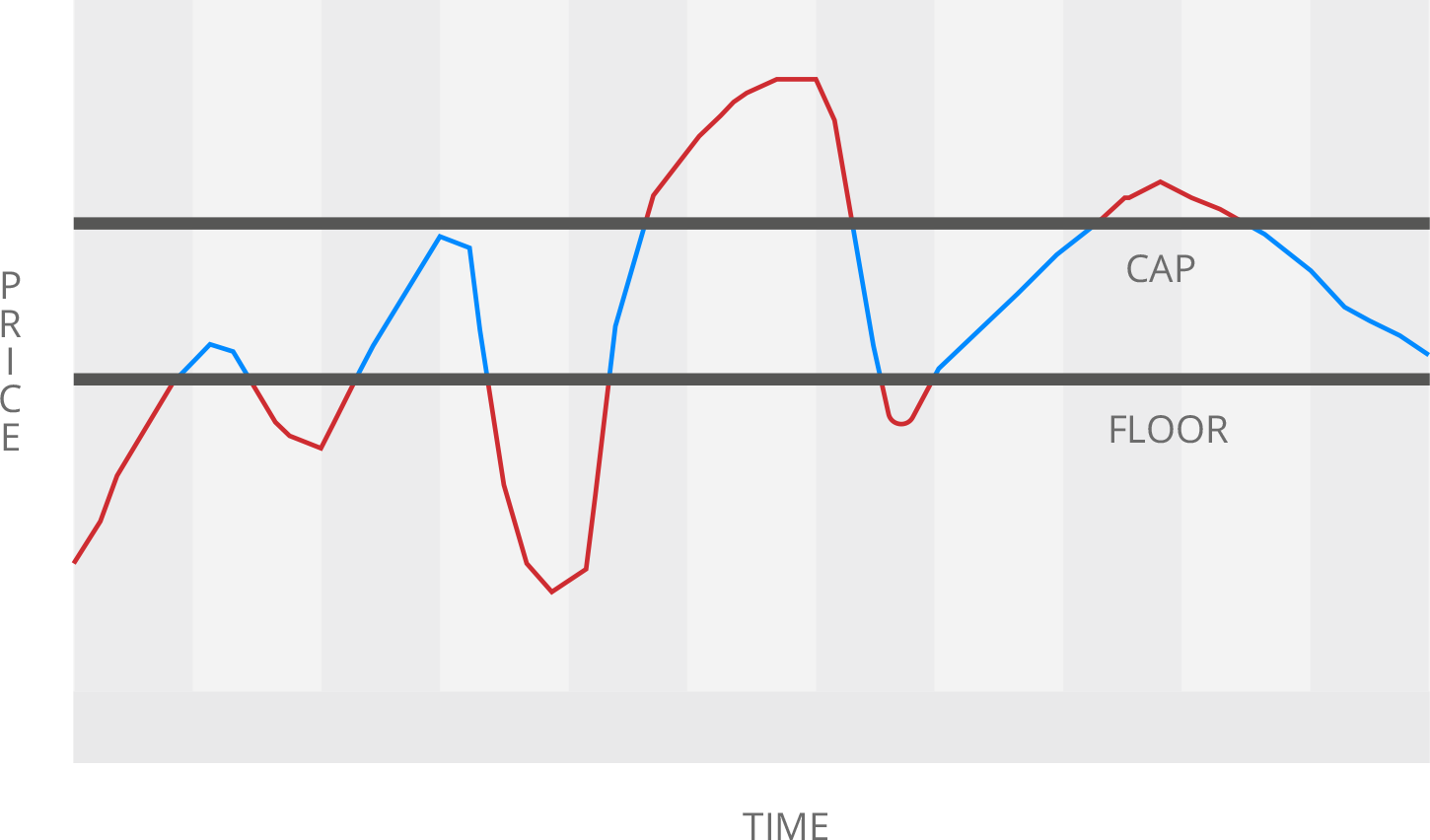

Collars and price floors caps.

Rate Cap Swap And Collar A Cheat Sheet To Managing Rate Risk Derivative Logic

Houston Astros Personalized Classic Leather Baseball Collar Leather Dog Collars Classic Leather Leather Collar

Make Your Own Dog Collar I Have Been Wanting A Bowtie Collar For Dexter But They Are So Expensive Dog Collars Leashes Diy Dog Collar Dog Leash

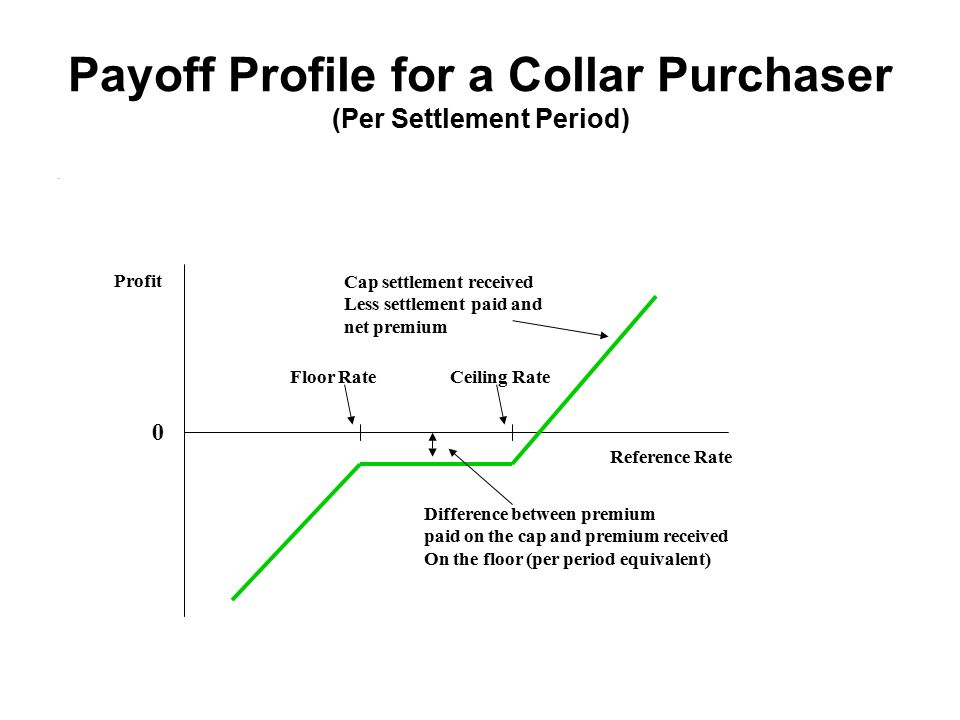

Caps Floors And Collars Ppt Download

Bright Orange Hunting Dog Collar Waterproof Dog By Doggonenice Hunting Dog Collars Waterproof Dog Collar Hunting Dogs

Inverted Cross Snapback Snap Casual Baseball Caps Hip Hop Cap Flat Hats

Custom Engraved Leather Dog Collar Side Release Buckle Purple Dog Pet Fashion Engraved Leather Dog Collar Leather Dog Collars Dog Collar

Lids Cap Care Kit Hat Cleaner Deodorizer Brush Water Stain Repellent Hat World How To Clean Hats Stain Deodorant

Overstock Com Online Shopping Bedding Furniture Electronics Jewelry Clothing More Energy Efficient Light Bulbs Floor Lamp Lamp

Pin On Ideas

Http Janroman Dhis Org Finance Bloomberg Capfloorcolar 20explained Pdf

Sodial R Digital Pet Collar Cam Camera Mini Video Recorder Cam Camera Dvr Video Recorder Monitor For Dog Cat Puppy Black Dog Training Techniques Dog Training Dog Training Tips

Semi Choke Martingale Collar Blind Dog Dog Pads Dog Leash

Brick Wall Print Design Floor Mat Wall Print Design Wall Patterns Brick Wall

Rockbros Winter Thermal Bike Headwear Neck Fleece Bike Caps Scarf Balaclava Windproof Warm Mask Motorcycle Bicycle Face Shield Velosiped Lyzhnyj Sport Maski

Hedging In An Uncertain Interest Rate Cycle Interest Rate Collar Derivative Logic

Women Mens Summer Cotton Berets Caps Casual Travel Sunscreen Visor Forward Cap Mens Summer Cotton Beret

Interest Rate Derivative Pricing Ird Valuation Caps Floors And Collars Swaptions Ppt Download

Sunnilook Orange Accessories Cashmere Accessories In 2020 With Images Womens Cashmere Cashmere Accessories Orange Accessories

Girls Heart Bracelet In 2020 Heart Bracelet Bracelets Rustic Cuff

20pcs Soft Cat Pet Nail Caps Claw Control Adhesive Glue Size M Cat Pet Supplies

Caprack18 Baseball Cap Hat Holder Rack Organizer Storage Door Closet Hanger Unbranded Cintres Chambre Enfant Decoration

Berdan S Sharpshooters Mcdowell Forage Cap Hat Xl Hats Caps Hats War Clothes

Options Caps Floors

Source : pinterest.com